Financial Distress in a Crisis: You Can’t Predict, You Can Prepare

Financial distress can quickly escalate during times of economic stress. What are the steps to take to protect against downside risks while preserving upside optionality?

Financial distress can quickly escalate during times of economic stress. What are the steps to take to protect against downside risks while preserving upside optionality?

Jeff is a graduate of Harvard Business School and Harvard Law School with experience in multiple industries.

Expertise

PREVIOUSLY AT

The COVID-19 pandemic has brought about unprecedented disruption to global economies. The financial and emotional fallout for governments, businesses, and citizens will persist long after the necessary isolation rules are relaxed, with talk already begun that the global economy will have its worst contraction since the Great Depression of the 1930s.

Since the duration and severity of the current economic crisis remain unclear, businesses must survive this downturn so that they can thrive in the eventual recovery. Turnaround consultants provide an experienced, outsider’s perspective and can help protect against downside risks while preserving upside optionality. Overall, you can’t predict, but you can prepare.

How Financial Distress Can Affect Your Business

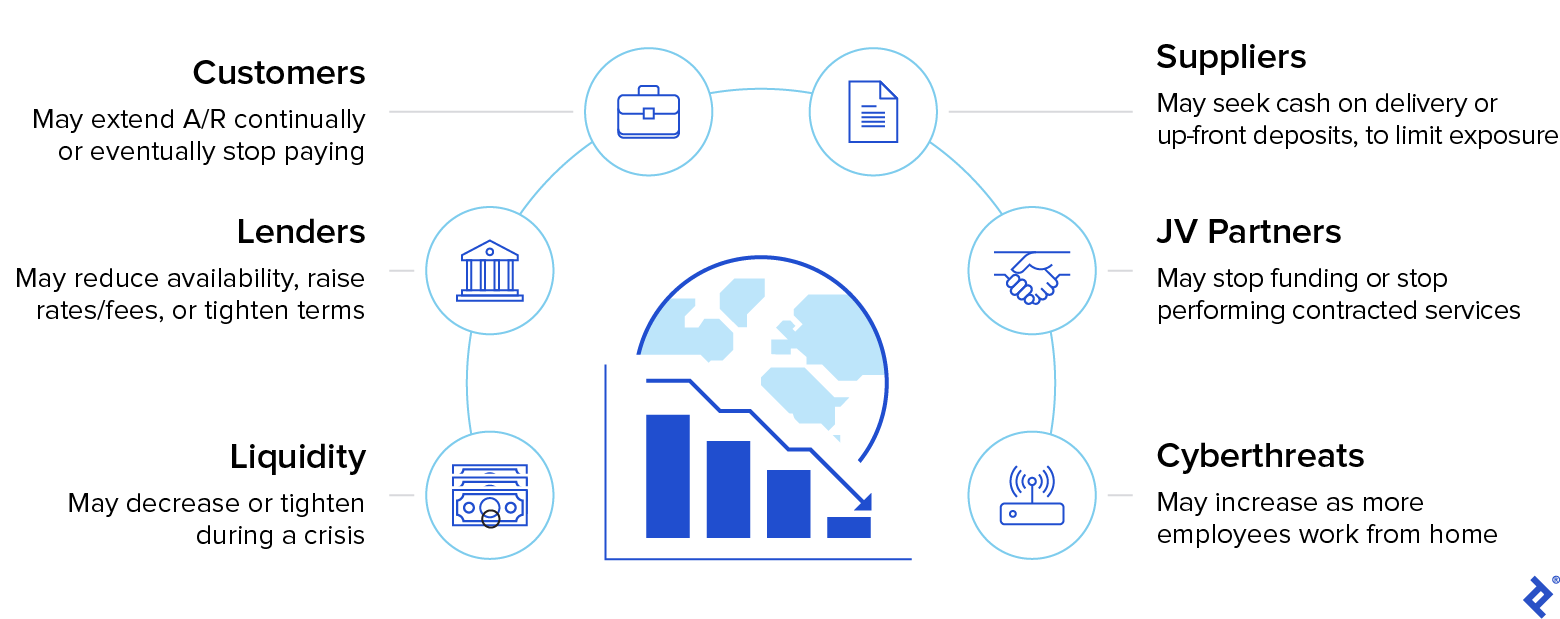

Even if your company is conservatively managed and well-capitalized, you can be adversely affected by the financial distress of others. As a turnaround consultant, I have seen many instances where the distress of key stakeholders trickled over to the client, causing their own eventual bankruptcy. Customers may default or stop paying, financially distressed suppliers can disrupt your supply chain, desperate competitors may cut prices to unsustainable levels, and banks and investors may pull back from funding. There are several actions that companies can take to navigate through this uncertainty and minimize their financial exposure.

Financial Considerations During a Crisis

The six areas that you can focus on are:

- Liquidity: More important than revenue and profits, focus on liquidity, liquidity, liquidity. Liquidity is how much cash you currently have on hand plus your ability to draw upon revolving lines of credit.

- Lenders: Banks will be hyper-focused on near-term cash flow and covenant headroom. Communicating with lenders is essential during any kind of financial crunch.

- Customers: Customers are the ultimate source of your cash flows. Avoid customer concentration, even if you sacrifice margins. As key customers become financially distressed, they will start paying later and later, and eventually not at all. Monitor your A/R aging report twice a week.

- Suppliers: In the short term, examine your supply chain and decide if you need to maintain some inventory buffers to mitigate potential supplier disruption. Dual source everything.

- Joint Venture (JV) Partners: Due to an unexpected change of circumstances, JV partners may be unable to meet their funding requirements or perform their contracted services. It is important to understand your rights if they stop funding so that you can decide upon the best course of action.

- Cyberthreats: Personnel turnover and working from home expand vulnerabilities for cybercriminals to attack. Make sure you have the proper procedures in place.

Hiring a turnaround consultant to address these issues can help a management team stay focused on day-to-day operations while entrusting delicate communications and challenging negotiations to professionals.

1. Focus on Liquidity: Hope for the Best, Plan for the Worst

Having a solid understanding of your company’s liquidity and cash flows is the #1 priority when adapting during a downturn. While a crisis like COVID-19 may seem like a temporary economic downturn, it may extend into a longer, more severe recession. Review the history of industry cycles in your field to calibrate the downturn’s severity and duration. Analyze your fixed vs. variable costs and calculate contribution margins (not gross margins) for each scenario. In periods of significant volatility, it is important to run multiple scenarios in parallel and develop a contingency plan for each. Create a detailed timeline for implementing each plan. If you’re unsure how to do this, a turnaround consultant can help.

Businesses need to have the financial discipline to objectively review past downturns and overlay what those conditions would do to your business today. Since survival depends more on liquidity management than revenue growth and profit margins, decisions must be made with liquidity constraints in mind.

When I was previously appointed as interim CEO of a large national company, my team and I managed the turnaround plan and focused on optimizing core operations and enhancing short-term liquidity. We prioritized cash collections and the availability of lines of credit to keep the lights on. We identified issues and built consensus with the senior management team and staff. Most importantly, we were proactive rather than reactive. In case of emergency, Plan B is likely to become Plan A, so it is important to do your homework ahead of time to ensure that liquidity and cash is on hand when needed.

2. Managing Lenders: Be Proactive and Communicate

Economic shocks inevitably signal upcoming financial defaults across industries, which will require loan amendments and forbearance agreements to avoid widespread bankruptcies. Having worked on both sides of the table, I understand the needs of both companies and lenders.

During uncertain times, banks tighten their policies by scrutinizing existing loans and triple checking new applications. In addition to liquidity, banks will be hyper-focused on near-term cash flow and covenant headroom, meaning the margin for error between actual and budgeted credit metrics is slim. Credit and workout teams now have much more say in scrutinizing borrowers and are demanding more analysis of downside scenarios from client relationship bankers.

To maintain a positive relationship with lenders during these uncertain times, it is important for you or your turnaround consultant to arm your bankers with realistic information on your company. Communicating with lenders is essential during a crisis; hiding problems now can ruin your credibility later. The key to managing lenders is to be proactive in discussing those well-quantified downside cases and action plans.

Turnaround consultants are pros at handling these delicate discussions where they share a thoughtful Plan A and a candid Plan B. Lenders understand that their borrowers are under pressure and experiencing a high degree of uncertainty. The more you can show your ability to manage thoughtfully and decisively in a downturn, the better the reception by your banks. Doing this will allow banks to spend more time with the less prepared borrowers - who will get much tougher treatment - and allow you to focus on what is really important, running your business.

3. Managing Customers: Analyze Receivables Aging Reports and Avoid Customer Concentration

Customers are the ultimate source of your cash flows, but beware of one key customer’s distress triggering your own distress. Whenever you sell products or services on terms, you become your customer’s unsecured creditor. Consider the effect of your key customers paying later and later, and eventually not at all. Remember that desperate times call for desperate measures, so even long-term relationships can change drastically in a financial crisis.

Customers in Distress

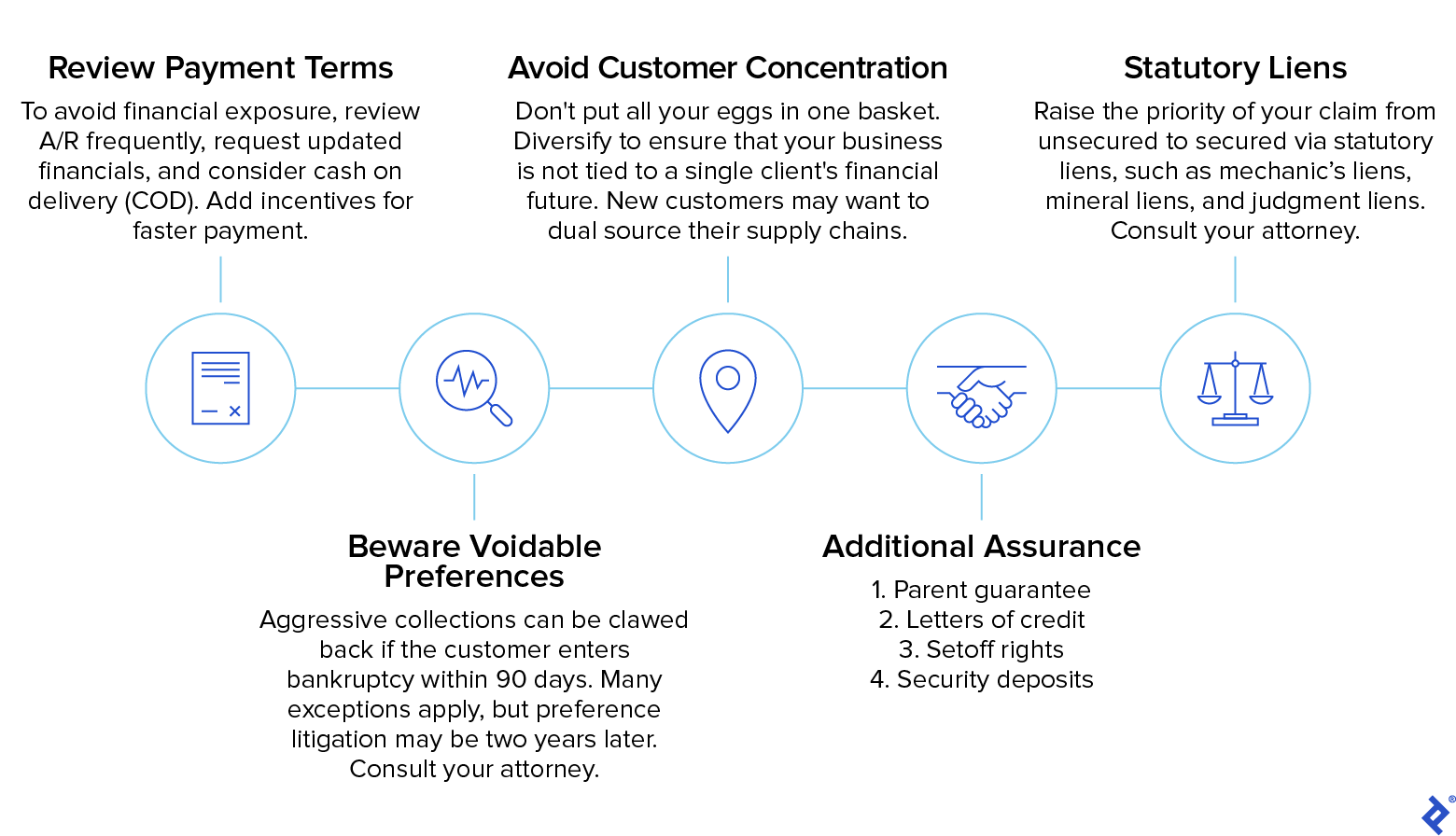

Now is a good time to perform fresh credit checks for all of your customers, including requesting updated financials. Additionally, consider a fresh review of all of your contracts and other legal documents with your customers. In particular, understand any force majeure or similar clauses where your customer could cancel contracts or alter terms.

You or your turnaround consultant should monitor your receivables aging report twice a week and watch for negative payment trends. Scrutinize receivables past due 30-60 days, 61-90 days, and over 90 days and look for changes in payment patterns for specific customers. I have often seen instances when customers who habitually paid in 45 days changed to 60 days or more. When you spot potential trouble, you should start communicating more regularly with these customers before small problems escalate.

Consider adding incentives for faster payment and be suspicious when new excuses keep arising. In particular, be more aggressive with collecting receivables that are past due 90 days or more and consider seeking legal advice for protecting your financial exposure, such as initiating litigation and filing a lien to become a secured creditor. In extreme situations, consider hiring a debt collection agency.

Spread Risk Among Customers to Reduce Concentration

Avoid customer concentration even if it comes with the sacrifice of margins. Remember, liquidity is more important than revenue growth and profit margins in a crisis. If you already have customer concentration, consider accepting new business from less attractive customers in order to dilute your exposure to one large customer. If that is not possible in the near term, consider merging with a competitor that has also concentration but with a different customer. For example, if 70% of your revenue comes from Walmart and 70% of your competitor’s revenue comes from Target, merging together would create a more stable customer profile and mitigate risks from a customer experiencing financial distress.

If your financial exposure becomes alarming as a particular customer starts paying later and later, consider having your turnaround consultant ask for cash on delivery (COD) for future orders. Balance the value of your long-term relationships with the risks of never getting paid after you deliver goods or provide services. Sometimes, you need to cut off a customer entirely until payment is made for prior orders. You can also request parent guarantees, letters of credit, setoff rights, and security deposits as extra credit support.

Be aware of voidable preferences and other legal risks. Aggressive collections can be clawed back if the customer enters bankruptcy within 90 days. If the customer slips into bankruptcy, you want to have your files organized promptly so you will be prepared for potential preference litigation, which may arise months or years later. Many exceptions apply so consult your attorney about voidable preference risk for your company.

4. Managing Suppliers: Mitigate Supply Chain Disruption

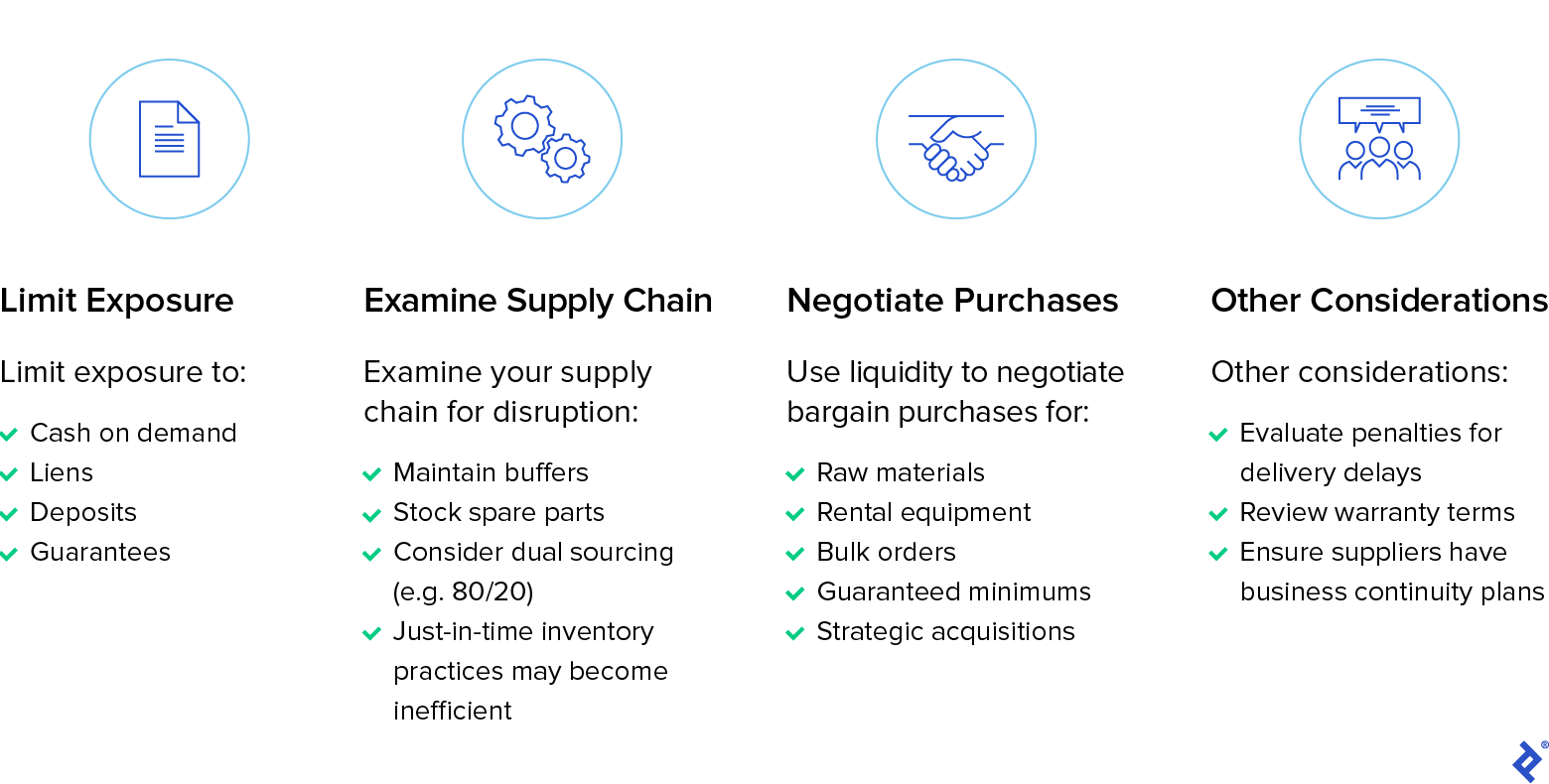

The biggest supplier risk is disruption to your supply chain, particularly if a supplier is the sole source or major source for important components. In general, it is best practice to dual source everything in your supply chain. Give alternative suppliers small orders to get your systems set up and the relationship established. If your main supplier experiences financial distress, you will have a backup ready rather than find yourself scrambling to find a replacement.

Suppliers in Distress

Turnaround consultants will examine your entire supply chain and decide if you need to maintain inventory buffers for raw materials and finished goods. They will also help you re-evaluate just-in-time inventory practices because expected efficiencies may create unforeseen problems if your supplier suddenly goes bankrupt. During uncertain times, just-in-time inventory practices may actually become inefficient.

Similarly, consider stocking spare parts for key equipment and machinery. Especially if the manufacturer or distributor is overseas, there may be costly delays in delivery. Avoid unnecessary emergencies by planning ahead. Unexpected downtime and surprise delays during a crisis can strain your liquidity unnecessarily.

Just like you may seek COD, deposits, guarantees, liens, etc. from your customers to limit your financial exposure, your suppliers may seek these credit enhancements from you. Therefore, you should try to maintain trust and strengthen relationships so that your suppliers continue to extend credit, especially if a supplier is critical for your business. If you already have a large deposit with a supplier, consider having your turnaround consultant ask to get some or all of it returned to increase your liquidity, even if it means paying higher prices or accepting COD terms going forward.

If you are fortunate to have ample liquidity, consider using your liquidity strength to negotiate bargain purchases from suppliers. As the customer, you may be able to purchase raw materials, buy used equipment (rather than leasing), obtain bulk orders for volume prices, or even make strategic acquisitions at a discounted price.

5. Joint Venture Partners in Distress: Take Proactive Steps

It is also worth refreshing your financial analysis of any JV partners and rereading related legal agreements. Turnaround consultants can help you review the Joint Operating Agreement (JOA) to plan for the effects of a worst-case scenario on your company’s liquidity. If your JV partners become financially distressed, they may be unable to meet their funding commitments or perform contracted services, meaning you may find yourself with an unexpected financial burden. To prepare for these unfortunate circumstances, it is important to understand your legal rights now so that you can decide upon the best course of action. Before taking any proactive steps, consult your attorney to understand your rights.

If JV partners change their outlook and stop funding or performing, you may have remedies under the JOA. The JOA may give you rights to:

- Enforce funding deadlines

- Exercise cash call rights

- Request deposits, parent guarantees, letters of credit, and other credit support

- Exercise suspension of rights, all of which your turnaround consultant can help you understand

Additionally, you may want to consider making direct payments to vendors instead of indirectly paying via the JV partner. Alternatively, you may want to deposit cash in an escrow account with clear instructions for an agent on releasing funds. Either approach helps prevent your cash from being trapped in a JV partner’s bankruptcy estate.

6. Cyberthreats Increase During Distress: Protect Your Company

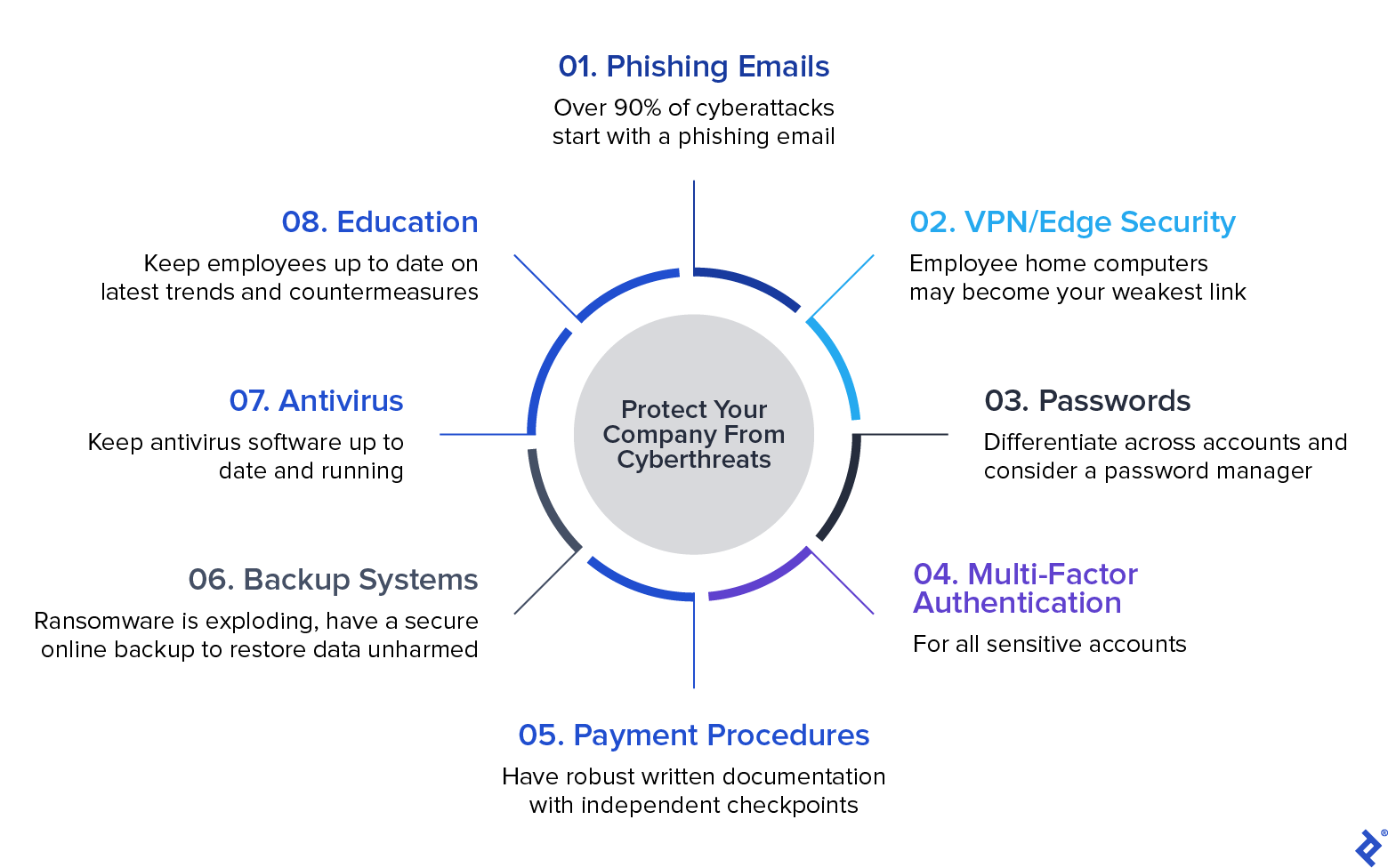

Finally, while many parts of the global economy are negatively impacted by the COVID-19 crisis, cybercriminals are one of the few groups who look to exploit it for benefit. From large publicly traded energy companies to small 10-person shops, I have seen cybercriminals indiscriminately send phishing emails to employees to try to send malicious malware or secure funds. During the swift transition to working from home, many companies are testing full-blown remote capabilities for the first time. Turnaround consultants can help you understand and revisit your policies, procedures, technology, testing, and training to ensure that employees’ (and if appropriate, external stakeholders) home computers are safe and secure from cyberthreats. You should understand the identities of all people who have access to your systems and ensure that adequate security is in place on their computers to protect from cyberthreats.

Protection Against Cyberthreats

Take a “zero trust” approach to any financial transaction and assume employees’ passwords are compromised. To prevent loss:

- Ensure two-factor authentication on ALL key accounts (banks, email, ERP system, etc.).

- Create failsafe procedures with independent checkpoints for all cash disbursements.

- Keep antivirus software up to date and running.

- Lastly and most importantly, train employees on phishing and keep them up to date on the latest sneaky threats and effective countermeasures.

Employees can be your weakest link or your strongest defense, depending upon how well you equip and train them to succeed.

You Can’t Predict, You Can Prepare

Turnaround consultants benefit their clients by bringing relevant experience in crisis management, practical insights for risk assessment, best practices in implementing rapid change, and proven ability to unravel intertwined financial, operational, and legal issues. Taking proactive steps now will prevent emergencies later. Delaying action will inevitably increase your company’s risks, transform small problems into large issues, and may result in a bankruptcy that could have been prevented.

All of these issues demonstrate that, while you cannot predict the ultimate effect of an unexpected crisis, you can take deliberate steps to prepare for downside scenarios. As seen in the examples throughout this article, during times of stress, it will be evident that other stakeholders to your business (e.g., your suppliers and customers) will also be going through hard times. An exceptional turnaround consultant is one that can both empathize with a range of stakeholders but also negotiate efficiently to manage their clients’ best interests.

Further Reading on the Toptal Blog:

Understanding the basics

What is a turnaround consultant?

Turnaround consultants help businesses navigate through tough operating conditions that have compromised performance. They identify areas of the business that can be improved - or mitigated - to assist its rejuvenation.

Jeff Anapolsky

Houston, TX, United States

Member since December 11, 2017

About the author

Jeff is a graduate of Harvard Business School and Harvard Law School with experience in multiple industries.

Expertise

PREVIOUSLY AT