2021 is winding down, and new year’s resolutions are in the air. The FRED team is also thinking ahead to 2022, when it will update its data repository to reflect the discontinuation of several financial data series and the new reliance on some replacement series.

This FRED news post provides the details of this transition. For example, 35 London interbank offered rate (LIBOR) benchmark rates produced by the Intercontinental Exchange (ICE) will no longer be calculated as of December 31, 2021. The Bank of England foretold this change in 2017 and is taking over the production of replacement series, including the Sterling Overnight Index Average (SONIA).

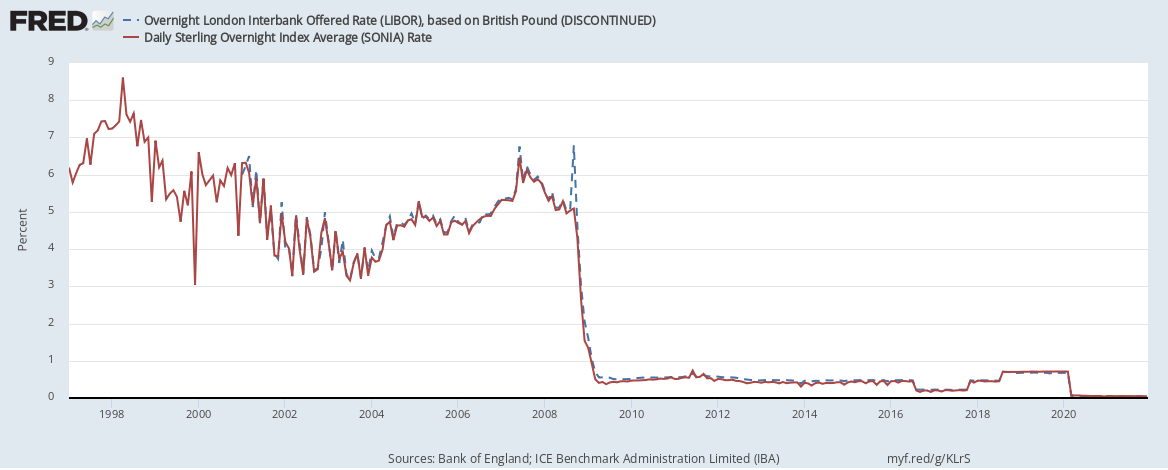

The FRED graph above shows the soon-to-be-discontinued overnight LIBOR in blue and its replacement, SONIA, in red. In short, both series are intended to reflect the interest rate at which banks could borrow money (denominated in British pounds, a.k.a. sterling) on unsecured terms in wholesale markets. The series are very similar in value, even though they’re calculated using different methodologies: LIBOR used a survey of large banks and SONIA is a trimmed mean of the relevant interest rates.

In the world of financial data, substituting one benchmark interest rate for another is a major endeavor. Know that FRED is at the ready to help data consumers adapt to these changes.

How this graph was created: NOTE: Data series used in this graph have been removed from the FRED database, so the instructions for creating the graph are no longer valid. The graph was also changed to static a image.

Suggested by Diego Mendez-Carbajo.