Why building trust and loyalty with passive investors is at the crux of real estate investing

December 1, 2022

Warren Buffet once said, “We never invest in anything we can’t understand”. Therefore, it’s imperative that you understand whatever you are investing in. When it comes to real estate syndications, you might be confused about terms like cap rate, DSCR, and equity multiple… So what does this real estate syndication terminology mean?

We spoke to many passive investors and got some insights on the most confusing terms for newbies. So this article uncovers all you need to know about real estate syndication terms, so when you read a deal, you can understand whether it is a good deal or not (hopefully). So let’s start from basics and then get into more complex terms.

This question is one of the most frequently asked by aspiring real estate investors. While minimum investment can vary per sponsor, typically it is $50,000 per limited partner. However, we’ve seen minimum investments as low as $25,000 and as high as $200,000. Why does it vary? There are three main reasons.

One of the first reasons is if the general partner is doing a 506 (b) offering, they will have a limit on the number of non-accredited investors they can attract to that real estate deal. According to SEC, the limit is 35 non-accredited investors per deal. With a minimum investment amount of $25,000, a deal sponsor will reach that limit quite quickly and, as a result, lock other potential non-accredited investors out of the deal.

Suppose that you are a deal sponsor raising equity for a $3M multifamily deal and your minimum investment is $25,000. In this case, you might end up with over 100 investors (hypothetically). Having this number of limited partners creates much more paperwork, follow-ups, administrative burdens, etc. Therefore, having a $50,000 minimum investment would make much more sense.

No reputed real estate syndicator would want their passive investors to invest their very last funds into a deal and would want their LP’s capital to be an insignificant portion of their overall net worth. Passive investors must invest capital that they don’t need to live on, so sometimes having a higher minimum investment amount, protects GPs from having “all-in” investors in their deal.

Now, let’s talk about a crucial document for passive investors – SEC PPM.

We know that when you are just starting to learn about real estate investing, it can be difficult to understand all the new vocabulary and learn about all the little, but crucial details that can help you make it or break it when investing in real estate. In this article, we will discuss SEC compliance for passive investors and what you can expect to see in an SEC PPM.

There are three main ways to invest money in multifamily properties. You can be a passive investor, a deal sponsor, or a so-called individual investor. You can also be two or all three of those simultaneously, like our Founder, Perry Zheng, who invests passively and sponsors deals as a GP.

Group purchasing of real estate involves passive investors (LPs) and deal sponsors (GPs). There is usually one deal sponsor (sometimes with one or more co-sponsors) and a group of passive investors.

The individual investor model usually involves one person or a couple buying a property with their own funds without raising money from other people.

There is no way we can cover everything you need to know about SEC in this article. However, we will give you an overview of what to expect to help you become a sophisticated investor.

SEC stands for Securities and Exchange Commission. A security in this context involves an investment of money into a joint enterprise with an expectation of profit. The anticipation of profit comes from the deal sponsor, meaning that passive investors trust that the deal sponsor will control the assets making day-to-day decisions. As a result, the profit will depend on the skills of the sponsor and how they make these decisions.

It means that the deal sponsor sells securities when raising money for a deal, and passive investors are buying securities. In the USA, you need to have a securities license to do this with a few exemptions.

They include:

Whether you are a passive investor or a syndicator, you need a specialized SEC attorney who advises you on all these details. Another important document you need if you are a deal sponsor is a PPM from your SEC attorney. Do not reuse or recycle PPMs from other properties because raising money with a plagiarized PPM is illegal.

Another critical point in the SEC law is that you aren’t allowed to do general solicitation or public advertising when raising money for your deal as a deal sponsor. It means that even soliciting investor information via your website is not permitted. A deal sponsor can’t ask strangers for money either because it’s considered a general solicitation.

The first step in building your investor database as a syndicator is to create “substantive” relationships with your investors. It means you need to have a detailed conversation to get to know some details about this person, their goals, what they do, their business, etc. Once you have substantive relationships, you can start soliciting. That’s why our real estate investor portal allows only for one-way discovery of syndicators so that they cannot solicit investors or poach other syndicators’ investors.

As a syndicator, you need to have a record-keeping system to track when you meet your passive investors, discussion notes, and meeting minutes.

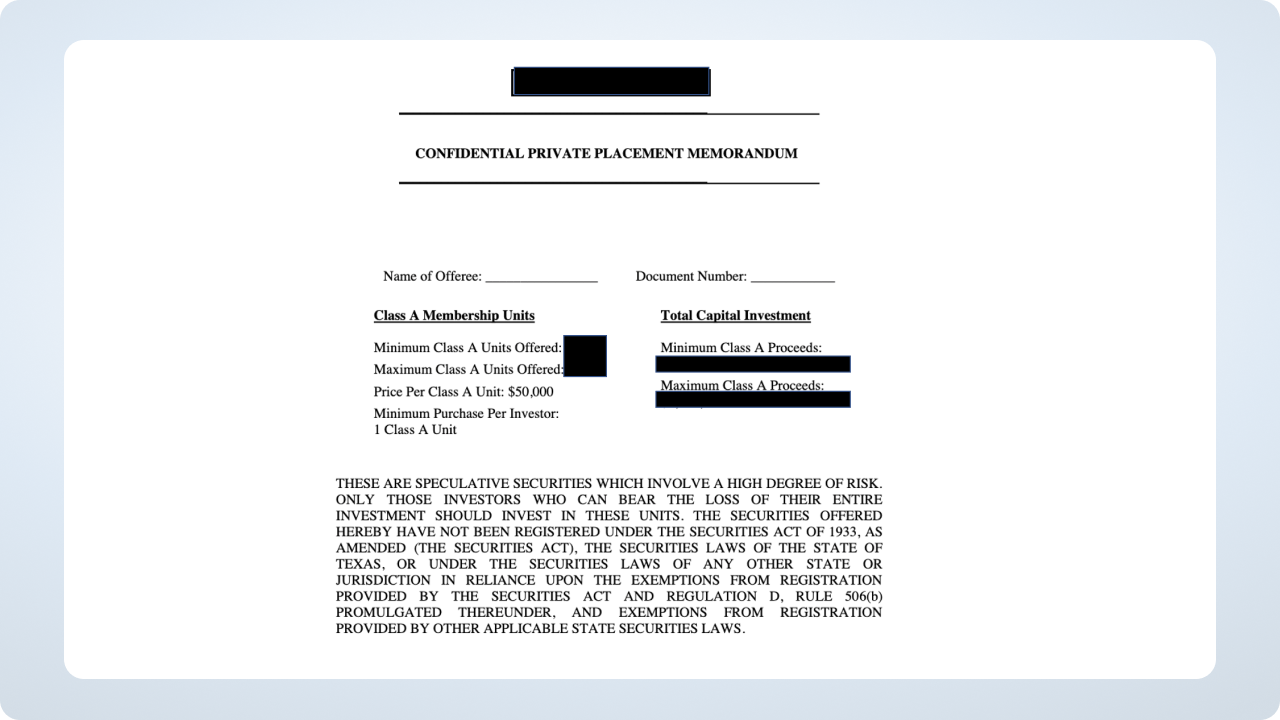

An SEC PPM is a legal document that companies file to describe a private offering of their business. The documents normally include detailed financial statements for the offering, including profit and loss statements, any third-party due diligence and analysis, and background information on the company’s officers and directors.

The first page would usually look like the one below. It will have the name of the LLC, the number of units offered in each class, the minimum investment (in this case, it’s $50K), and the total capital investment.

SEC PPMs are 50+ pages long, and here is what they usually contain:

The risk factors section is a mandatory requirement by SEC, and it demonstrates all the risks that investors might face by investing in this property. This section can be anywhere from five to thirty pages. As a passive investor, it is your responsibility to familiarize yourself with these risks before making your investment decision.

The first and essential part is the summary and terms of the offering. It contains information about the deal, the Manager, the Manager’s fees, minimum investment, and the number of unaccredited investors to which the company can offer this investment. The Manager, in this case, is not the property manager. It is the Manager of the LLC (typically, the deal sponsor).

Now, let’s dive into the real estate syndication structure.

There are different syndication structures depending on the preferences of the general partners, their track record, experience, and the market. As a passive investor, you need to examine the syndication structure, regardless of asset and market class, and ensure that this structure aligns with your investing goals.

Two main types of syndication structures are:

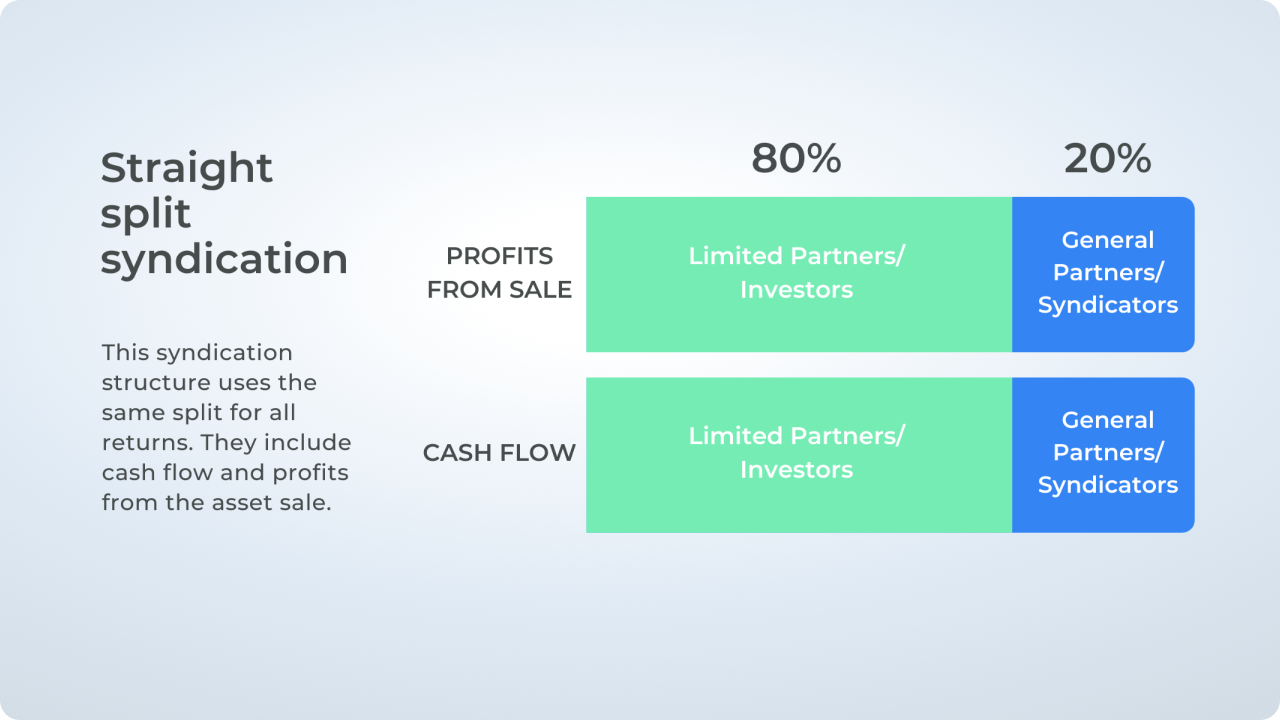

A straight split is the most straightforward structure to understand. It uses the same split for all returns, including cash flow and profits from the asset sale.

Here is a visual example of an 80/20 split.

In this example, 80% of cash flow and profits from the property sale go to limited partners or passive investors, and 20% goes to deal sponsors or general partners.

When profits from the investment asset sale are high, this structure can be especially beneficial for limited partners. For example, on a gain of 40%, a straight split on a $50,000 investment would get you 80% of $20,000 or $16,000.

In a straight split structure, you will likely see fewer benefits from cash flow distributions than with the waterfall structure discussed next. So if you are looking for more ongoing passive income, a straight split might not be for you.

The waterfall syndication structure uses preferred return, and many passive investors love it.

In this structure, investors receive preferred treatment for the first % of the preferred return. For example, you invest $50,000 into syndication with a 7% preferred return, and in the first year, the returns are 7%. It means that you get the full 7% preferred return on your original investment, or $3,500. Deal sponsors don’t get any returns.

The waterfall structure does not guarantee that investors receive the full 7%. However, it ensures that investors get preferred treatment for the first 7% of returns. As a result, deal sponsors are under a lot of pressure to get returns to surpass 7%.

Once deal sponsors reach this threshold, it activates a different % split. For example, any returns between 7% and 14% might be split 70/30 – 70% to passive investors and 30% to deal sponsors. After hitting the 14% threshold, the split changes again. Sometimes to a 50/50.

This structure ensures that deal sponsors take on an asset only if they are confident that it will generate returns above the preferred. Moreover, this structure motivates them to work hard and make the investment perform at its best.

The better it performs, the more returns passive investors get, and the more deal sponsor gets. A waterfall structure is also best if you are looking for a stable source of passive income.

This structure usually brings fewer profits at the sale of the property for passive investors.

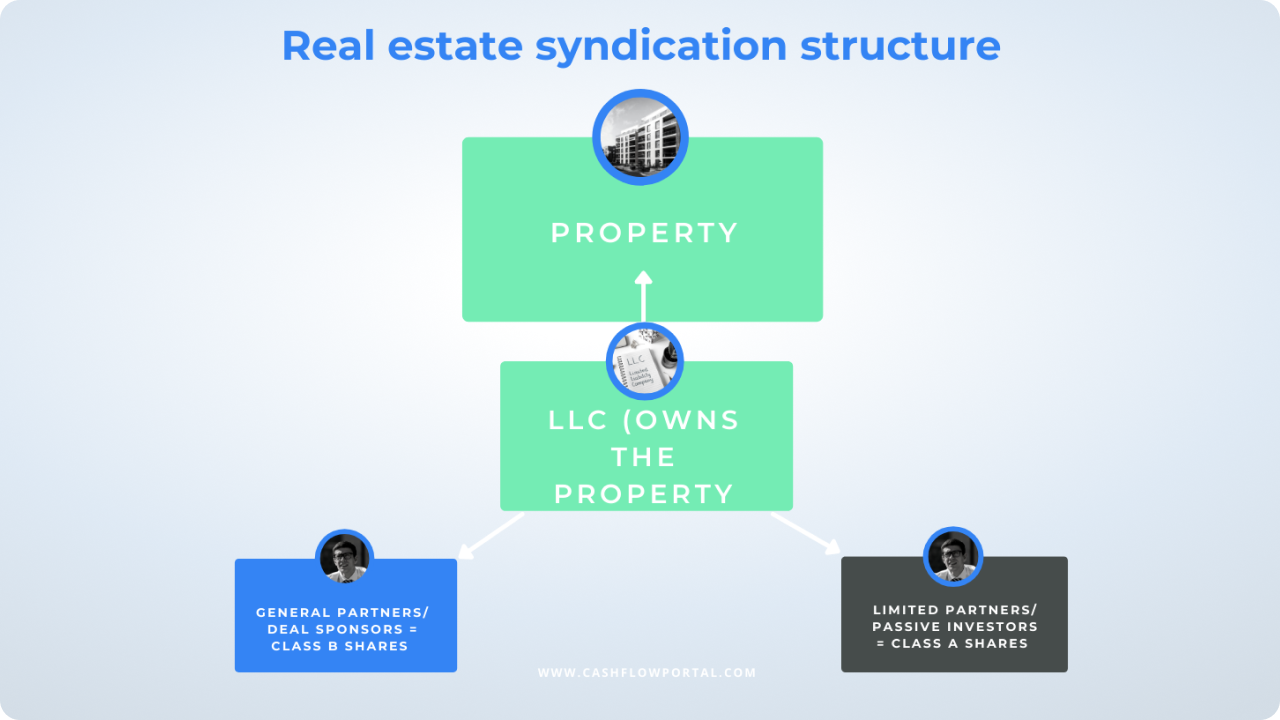

This is how syndications are usually formed:

It’s important to highlight that in real estate syndication, nobody owns the property because an LLC owns it.

The syndicator needs to consider the type of money they are going to raise because it will dictate what type of PPM (private placement memorandum) and other types of documentation they will need when fundraising.

Usually, the structure of real estate syndications looks like this:

There are two common classes of shares that are sold by the syndication. Usually, you will see:

Deal sponsors invest sweat equity and are also responsible for investing anywhere from 5% to 20% of the total equity. As a passive investor, you want to see deal sponsors invest substantial equity in the deal.

Now that you are familiar with the basics of multifamily syndications, let’s dive into some crucial terminology that you will encounter once you decide to invest in a syndication deal.

Cash on cash return, the annual rate of return, and the internal rate of return are crucial terms for those wanting to invest in real estate syndications. However, these terms quite often sound confusing and scare many new investors off. Let’s clear up the confusion.

The average annualized return or ARR is a metric used to calculate the average amount of revenue an investment brings each year. You can calculate the ARR by taking the total return on investment (ROI) and dividing it by the years of your investment: ARR = Total ROI/ number of years of investment.

Suppose you invest $50,000 in a real estate syndication, and your total ROI over four years is $32,000. In this case, ARR = $32,000/4 years = $8,000 average annual return. This number is an estimate of what you would earn each year that your funds are invested into a multifamily deal.

When a syndicator presents an investment opportunity to passive investors, he gives you an ARR as a percentage. For example, you might see a deal where you invest $50,000 with an estimated 16% ARR. Then, to figure out what that means for you in dollars, use the following example:

$50,000*16% = $9,461/ year

If your goal as an investor is equity growth, then, in fact, you may not see that $9,461 in your bank account every year. In this case, you might get a lump sum payout at the end of the syndication deal lifecycle, equal to an ARR of $9,461/ year, but paid at once.

ARR of 14% and higher is considered good for a property that needs only light upgrades. If you are looking at projects that need heavy value-adds, an ARR of 16% and higher would be considered acceptable. Although multifamily syndicators actively use this measurement, as a passive investor, you should focus on IRR more because the ARR does not consider a variety of factors, including time and opportunity cost, inflation, etc. So let’s talk about IRR.

The internal rate of return is a metric used by many industries, not only real estate. The IRR determines the overall rate of return by comparing the sale price, the purchase price, and the yearly cash flow. The crucial aspect of IRR is that it takes into account the time value of money, an essential concept in finance. The time value of money quantifies how much value is in the investment.

When looking at real estate investment properties, investors often evaluate real estate deals by their IRR (internal rate of return) along with other metrics. This metric helps investors understand the potential upside of an investment property. Moreover, IRR also determines real estate sponsor promote.

Why is IRR important for real estate? Let’s talk about this statistic in detail.

A lot of people get confused between IRR and ROI. The difference is straightforward: ROI calculates the growth of your investment over the total period, and IRR calculates the annual growth.

In real estate investments, IRR estimates the average annual return that a property has yielded or will yield over a specific period. This number is calculated as a percentage, and you can use it to compare the IRR you forecast to receive in real estate against the IRR you may receive in another kind of investment. IRR calculation must be done during your due diligence, along with other statistics.

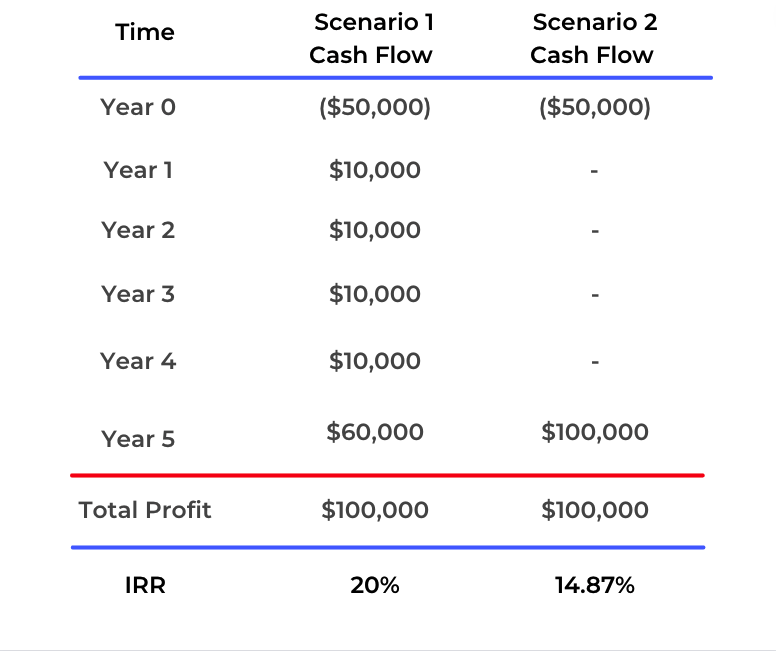

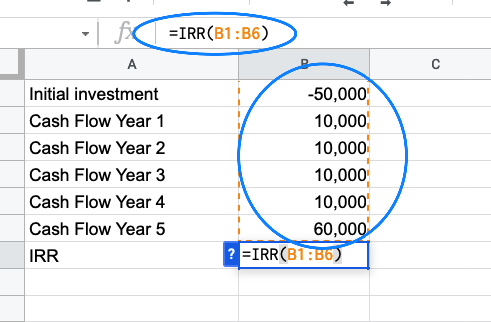

Because IRR measures the time value of money, it tells you which initial investment will bring you better returns because 30% ROI in 3 years is not the same as 30% ROI in 10 years. Let’s look at this example:

In this example, both scenarios have equal profits. However, in scenario No 1, an investor received the profit incrementally over the 5-year hold period. In the meantime, in scenario No 2, you don’t receive any cash flow throughout the hold period, and you get all your profit along with your principal at the end of the entire holding period of 5 years.

At first glance, it may seem that both of these scenarios are equally profitable. We’ve calculated IRR using an Excel formula like this one:

We can see that scenario 2 has a lower IRR because there is no cash flow. Cash flow offers you an opportunity to reinvest it somewhere else and generate even more returns with that capital. Therefore, there is an opportunity cost that you need to take into account when evaluating investments. As a real estate investor, you should be looking at IRR in addition to cash on cash return and equity multiples.

There are several crucial components involved with IRR calculations in real estate and here is the formula that expresses those components:

N = The total number of hold years

Cn = The cash flow in the current period

n = The current period

r = The internal rate of return

It’s essential that you understand these statistics to comprehend IRR fully.

Net present value is the difference between the present values of all cash outflows and all cash inflows. NPV indicates whether your investment is achieving a target return at a specified initial investment. NPV also tells you what adjustment you need to make to the initial investment to achieve the target return, assuming everything else remains unchanged.

To calculate the NPV, subtract the present value of cash outflows from the present value of cash inflows.

Above, we mentioned opportunity cost, also known as the discount rate. Let’s say you can earn 10% a year on your cash guaranteed. In this case, your discount rate would be 10%. Ten-year Treasury bonds are considered risk-free investments and can generate cash. Therefore, investors often compare the discount rate against a ten-year treasury bond. Generally speaking, your real estate investment comes with risk and must be above any guaranteed return.

Cash flow is the amount of money your real estate investment generates for you each year (distributions). For example, if you invested in a real estate multifamily deal and receive $5,000 every three months in distributions (rent income), you have a positive cash flow of $20,000 a year. If you are using our real estate investor portal to manage your deals, you will see this chart with a cash flow history that helps you understand whether your deal generates positive cash flow.

In general, a high IRR tells you that the real estate deal might be worth investing in and helps you evaluate real estate investments. However, IRR alone doesn’t take into account future expenses, property appreciation, and risk tolerance. Let’s take a look at the limitations of IRR.

Cash on Cash is a measure of real estate performance or what you can expect to get out of your real estate syndication investment. Basically cash-in vs. cash-out. It equals annual pre-tax cash flow, divided by the total cash that you put into the investment. It’s an important ROI, but keep in mind that cash on cash doesn’t give you a holistic idea about the value of your investment property and what you would get if you held it through the entire period. It only takes into account one year at a time.

Cash on cash return is more important than IRR if you are investing in a property with 10 units or less, because, in this case, IRR becomes less relevant. However, cash on cash return shows you your annual ROI, which IRR does not give you. So both metrics are important when used together.

Take your cash flow and divide it by your initial investment. Your initial investment should include all the funds that you’ve invested into the deal. Cash flow is calculated by taking all the rents in and subtracting the expenses. Expenses include mortgages, taxes, insurance, management, capital expenditures, etc. For example, you’ve invested $100K into a deal, and in the year one of the investment you earned $7K. In this case, the CoC for year 1 is 7%. It’s not uncommon for the Cash on Cash return to change as general partners implement value adds, property improvements, and increase rental rates.

When looking at a multifamily syndication deal, you will usually see a 5-year hold period and a cash-on-cash return rate in % next to each year. You might also see a CoC for disposition below the initial CoC. Disposition means selling the property. So it’s your cash-on-cash return based on the sale profits. It’s common to see one rate of CoC over the hold period and then to see a completely different figure (sometimes over 50%) for disposition.

Another essential term for passive investors is equity multiple. Let’s discuss what this term means for you as an investor and how it can help you review potential real estate deals with more confidence, allowing you to compare projected returns across multiple deals. As a result, you will make wiser investment decisions.

Equity multiple is the amount that your capital or your equity will be multiplied over the course of the projected hold time:

Your capital X Equity multiple = your total returns during the hold time.

Suppose a commercial investment property deal had an equity multiple of 2X over a projected hold time of five years. In this case, you could expect to double your initial cash investment within this hold time.

Equity multiple considers cash flow distributions throughout the project and the returns when the real estate asset is sold. So, if you invested $50,000 into a real estate deal that has a projected ARR (annual rate of return) of 10%, you will get approximately $5,000 per year for five years, equalling $25,000 in cash flow distributions over the hold period.

Once the investment asset is sold, you will get your original investment of $50,000 back, plus, approximately $25,000 in profit. So when you calculate your $25,000 from the cash flow distributions, plus $25,000 from the sale, you get $50,000 in total returns. You started with an initial amount of $50,000 and you ended with $100,000, therefore having an equity multiple of 2X.

Most syndicators aim for an equity multiple in their deals. However, remember that as with any projected returns, equity multiple is projected, meaning that the actual returns might not hit or far exceed this number.

Best practices can vary from country to country. However, in this post, we will be talking about the USA-specific standards for multifamily syndications.

December 1, 2022

October 31, 2022